March 2026: Crises present an opportunity to buy at depressed prices

On February 28, 2026, US and Israel armed forces launched airstrikes at multiple sites and cities across Iran. The conflict is now a month old. While there are many claims and counterclaims from both sides, the conflict has already, at 4 weeks, stretched beyond Donald Trump’s calculations who had earlier talked of a 4 week war. Bloomberg put up a headline on 11 March 2026 saying, “Iran’s cheap, plentiful weaponry puts US military under unprecedented strain”. It is an interesting choice of words and there are other articles in the US press which say that many of the US bases in the region have been hit, besides hits on oil facilities in the region. All in all, it has been a tough campaign, with Iran continuing to keep closed the important Strait of Hormuz and thus disrupt almost 20% of the total oil supply in the world, besides curtailing the supply of gas, fertilizers and helium (which is needed for making computer chips).

Most market participants expected the war to be over quickly as it pits the strongest military capability into war with a relatively weaker counterpart. Iran’s resilience has surprised many and there are some commentators who are even suggesting that Iran may have the upper hand, at this point, in the conflict. While this may or may not be true, it is clear that there is no clear winner 4 weeks into the war and there is a possibility that timelines of the war may stretch. The conflict has had the obvious impact on oil prices which have shot up higher and there are shortages of gas in many countries in the world, including India where it is being prioritized for domestic cooking purposes and commercial establishments are getting much less than their requirement.

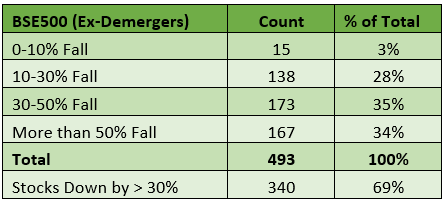

As we have noted in past newsletters, the Indian market was anyway on a downward drift, and the downward momentum got more legs due to the Iran war and the resultant impact on oil prices and gas availability which are key vulnerabilities for India’s macro situation. The table below shows the fall from All Time High (ATH) of the BSE500 constituents. 69% of the stocks are down more than 30% from their ATH and the median stock is down 40.1%. 34% of the stocks are down more than 50%.

Download BSE500 (Ex-Demergers) data (0% Fall – More than 50% Fall) (Excel spreadsheet, .xlsx)

The global markets have also been impacted by the Iran war, and the S&P is down 9.1% from its ATH while the Eurostoxx50 is down 10.2%. There are also growing concerns around whether the capex committed to AI is so large that returns from this capex in terms of revenues and profits may not be adequate to justify the large capex. Parallelly, the newer models like Claude Cowork and others are causing massive disruption to the Software as a Service (SaaS) companies – or at least to their stock prices. The world is still divided and unsure about how exactly AI will play out for businesses and enterprises in different sectors. In this context, we present below a table of how much each of the Magnificent Seven companies are down from their ATHs. The Nasdaq100 is down 12.3% and the S&P is down 9.1% from their respective ATHs.

Download Company’s (Last price and All Time High price) data (Excel spreadsheet, .xlsx)

So, as we can see, Mr. Market is not in a cheerful mood. Stocks are down in an almost indiscriminate fashion, and we have observed in the past that in such situations, the baby gets thrown out with the bath water. The spectrum of opportunities are increasing immensely in our chosen universe of high-quality companies. At times like this, cash infusion from clients would be most welcome because it allows us to buy at depressed prices, which would improve client XIRR over the long term. We all know from past memories that crises often present good opportunities to invest for the long term. It is the rare person who translates those past memories into action, who benefits in the long-term game of investing.