November 2025: Corporate results improving a little but valuations remain elevated

In this newsletter we discuss the results of the September 2025 quarter for the non-financials among the BSE500 constituents in terms of their revenue and EBIT growth. Below we present the results:

Revenue growth on 1Y basis is 7.5% and there is a strong growth in the EBIT for the September 2025 quarter though a large part of the growth is because of strong performance of the energy sector, where the oil PSUs reported very strong performance. If we exclude the volatile energy sector, revenue growth is 10% and EBIT growth is also 10%. For the June 2025 quarter, we reported ex-energy sector revenue growth of 7.6% and EBIT growth of 7.3%. To that extent, the September 2025 quarter is showing an improving trend. The EBIT growth for 3Y and 6Y basis (we have chosen 6Y instead of 5Y so as to eliminate the impact of covid on the numbers) is also reasonably strong at 14% each.

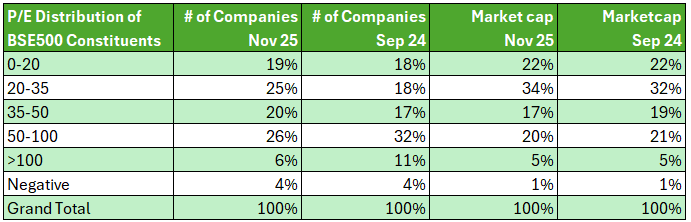

The Nifty scaled a new all time high in November 2025 on an intra-day basis. The last 12-14 months have been a period of consolidation for the Nifty. The median stock in the BSE500 is down 8.8% from its high on 27th September 2024. We now look at the distribution of Trailing Twelve Months (TTM) Price to Earnings Ratio (PE) among the BSE500 constituents and compare the same with September 2024 numbers.

In September 2024, 47% of the BSE500 constituents were trading at a PE higher than 50. In November 2025, that number has come down to 36% and in general it appears that the market is a little less expensive than the egregious levels it was trading at in Sep-24. The median PE of the BSE500 constituents has come down from 43.7 in Sep-24 to 35.9 in Nov-25. This is partly because of some earnings growth over the last year and partly because the median stock in the BSE500 is down 8.8%. Although the median TTM PE has come down from 43.7 to 35.9, the median market valuations at 35.9x earnings are still elevated.