HDFC Bank and HDFC Limited have been a core part of our portfolios for several years and both fit perfectly with the criteria that we look for in great companies – predictable and consistent growth, large addressable market opportunity, highly profitable and well managed. Earlier this month, it was announced that HDFC Limited will merge with HDFC Bank. HDFC Limited shareholders will get 42 shares of HDFC Bank for every 25 shares held. The final merger, if approved, will take 12-18 months to be completed as there are multiple regulatory approvals required. Given the implications, we thought it would be an appropriate time to analyze the merger, its implications and the core thesis for the investment itself.

The Indian banking industry, as measured by its total asset base, has been growing at 10.6% p.a. over the past decade – slightly above nominal GDP growth rate of 10.0% p.a. Private banks have been growing at a much higher rate of 16.5% p.a. over the same period. HDFC Bank has been growing at an even higher rate of 20.2% p.a. over the same period. Market share of private banks has increased from 19.5% to 32.8% over the past decade and the public sector banks have steadily lost market share. HDFC Bank has increased its share from 3.9% to 8.9% in the same period. Given these trends, it is expected that the banking growth will continue in India for the next several years, as banking penetration relative to GDP is still significantly lower than global averages. Private banks should continue to gain share and HDFC Bank should continue its relative share gains due to its strong franchise and risk management systems built over time.

A bank typically lends to both businesses and individuals. One of the largest pool of demand for loans is the home loan segment to individuals. Adjusted for the risk, it is a highly profitable segment and the repayment period is long, leading to a stable loan base. Home loan-to-GDP ratio in India is only about 11.4%, whereas the corresponding number in developed markets averages 40-80%. When HDFC Bank was originally incorporated 1994, it was agreed that HDFC Bank will not get into the home loan segment as the business conflicts with its parent’s business. HDFC Bank sources home loans for HDFC Limited and is also allowed to purchase a certain proportion of these loans. With HDFC Bank emerging as a dominant bank in India, it can continue to grow above industry by having access to the home loan market. Mortgage linked loans as a proportion of total advances for HDFC Bank was just 10.5% compared with 33.2% for ICICI Bank and 19.8% for SBI.

On the other side, HDFC Limited which is a pioneer in the mortgage business had a slight disadvantage due to higher cost of borrowing compared with the banks, as it was dependent on wholesale borrowing. Banks offer current and savings accounts to their customers, where the interest rate paid out is lower than fixed deposits and wholesale borrowing, leading to a lower overall cost of borrowing. With the merger, the advantages are clear – HDFC Bank will be able to lend to the home loan market and cross-sell banking products and services to the larger, combined customer base, using a lower cost of funds than HDFC Limited.

From a shareholder perspective, HDFC Bank has delivered a 23.0% p.a. stock price return over the past 20 years, which is 63x the original capital and so did HDFC Limited, with a 19.3% p.a., delivering significantly better returns than the Nifty at 14.8% pa. These returns are also in line with the underlying growth in these businesses. In terms of future prospects, given the underpenetrated nature of banking in India, private sector banks increasing its share and HDFC Bank being in an even better position post the merger, future growth prospects look very attractive.

Shareholder experience in the short term has been very different from the long term picture. Over the past 2 years, the Nifty has delivered a 31.7% p.a. return compared with 17.6% for HDFC Bank and 7.9% for HDFC Limited. HDFC Bank did face several internal pressures. RBI had clamped down on any new issue of credit cards till certain control systems were put in place. There were restrictions on opening current accounts with firms which had a loan with another bank. The explosion in use of UPI led to high levels of failures. There is also an increased regulatory oversight. HDFC Limited was also facing increased competitive pressures from other banks. We believe most of these regulatory and technology related issues have been fixed. The merger also addresses the competitive pressure faced by HDFC Limited. Despite these pressures, HDFC Bank has grown at nearly 18-20% and HDFC Limited at about 12% over the past 12 months.

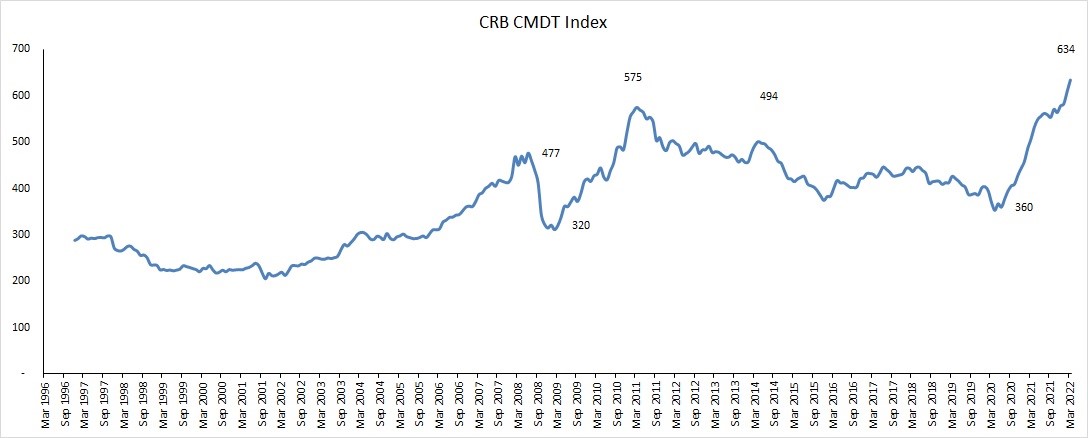

At current prices, HDFC Bank trades at close to 17x forward price-to-earnings which is much lower that its historical average of 22x. For most of the past 20 years, HDFC Bank has traded at a premium to the market whereas it is currently trading at a discount to the Nifty PE of 22x. One of the main reasons for this discount is the incessant FPI selling since October 2021. Of nearly Rs. 272,000 crores, a significant majority came from the BFSI sector. Never in the Indian stock market history have we seen such huge selling. Both HDFC Bank and HDFC have faced the brunt of this selling. Both stocks also went up sharply on the day of the announcement, but gave up all the gains. In the short term the cumulative holding in both these stocks has become disproportionately large for many institutional investors. HDFC Bank and HDFC Limited respectively account for 8.5% and 5.7% of the weight in the Nifty. Post-merger, their cumulative weight in Nifty will be closer to 12%, but as per Mutual Fund regulations a fund can’t hold more than 10% in a single stock. Merger of 2 entities also has short term implications on some other indices.

In the long term, stock market return from individual stocks depends on the earnings growth that the company can generate and the absolute valuations at which the stock trades. Even prior to the merger announcement, both the companies were on a strong growth trajectory with one of the best in class balance sheets in the sector. The merger will benefit both businesses in the long term. The stocks are also trading at a discount to both the market and their own historical valuations. The stock price weakness does seem temporary – especially given the spectacular track record over decades. Given the size of the holdings, one may need to fine tune the overall holding over time, but we have time to rebalance and till then both growth and valuations are in our favor.